What we do

People & Organisation

Change Management

Employee Experience

Leadership

Organisational Development

Talent & Development

Discover all services

Process & Performance

Analytics & AI

Operational Excellence

Process Management & Agile

Supply Chain Management

Strategy

Customer Experience

Digital Transformation

Growth & Acceleration

Policy Crafting

Strategy & Business Models

Value Based Healthcare

Sustainability & Circular Economy

Circular Economy

Climate Impact

Sustainability Excellence

Discover more

For whom

Private sector

Banking & Finance

HR & Social services

Utilities

Logistics & Transportation

Retail

Telecom & Media

Discover more

Education

Food & Beverage

Chemicals

High tech & SaaS

Building Materials

Healthcare

Health Policy

Primary Care

Hospitals

Life Sciences

Discover More

Society

Local Government

Regional Government

Federal (and European) Government

Discover more

Cases

Insights

Events

About us

Jobs

Contact Us

English

Nederlands (België)

Nederlands (Nederland)

Français

Home

Insights

Insights

Searchresults for

All services

Strategy & Business Models

Growth & Acceleration

Customer Experience

Employee Experience

Sustainability & Circular Economy

Process Management & Agile

Value Based Healthcare

Change Management

Operational Excellence

Analytics & AI

Supply Chain Management

Leadership

Organisational Development

Network Consulting

Cost Management

Sustainability Excellence

Value4Health

Climate Impact

Services

All industries

Private Sector

Healthcare

Publieke Sector

Industries

All types

Article

Video

Webinar

Mini-Guide

Types

Reset filter

Search

Search

Article

How can you improve your business with process mining?

What is process mining? How can it benefit your business? And what is the advantage of using process mining in business process management (BPM)?

Video

Rewatch the Lean Japan Tour - info session

Whether you're new to lean principles or seeking to elevate your organisational performance, this session clarified how the tour can benefit you.

Simplifying sustainability with the right ESG tools and how to choose?

Learn how to choose the right ESG tools and software for your business. Join the Sustainability Excellence Network and navigate common challenges.

Article

The power of scenario planning when facing uncertainty

Scenario planning: a (not so) obvious solution to decision-making in an uncertain world.

7 reasons to choose a consulting career | Möbius Insights

Are you a recent graduate looking for a rewarding career path, or an experienced professional seeking new challenges? Consider a career in consulting!

Article

Large-group facilitation: dialogue, insight and scaled action planning

Discover the power of large-group facilitation! Learn how this approach facilitates dialogue, insight and action planning with large groups of people.

Article

11 tips to improve team collaboration

Discover 11 practical tips to improve collaboration within your team and ensure more productivity, creativity and better team performance.

Article

Unlocking the potential of employee experience for business success

Discover the crucial role of employee experience in achieving your business goals, with insights on how to measure, improve and benefit.

Article

Process optimisation: get better results with higher efficiency

Learn about how process optimisation can help companies improve efficiency, productivity and performance, and find out how Möbius can help.

Operational excellence: Strategies for sustainable success

Achieving operational excellence is crucial for long-term success and resilience. Learn how to improve processes, drive efficiency, and boost business.

Article

Boosting business success through employee engagement

Discover the importance of employee engagement and strategies to increase it. Learn how engaged employees drive organisational success.

Article

Performance management: crucial for organisational success

Discover how performance management plays a crucial role in improving individual performance and organisational success.

Article

KPIs are dead, long live KBIs!

It is all very well having nice tools; however, it is the behaviour of the leaders and the employees that will determine the final results.

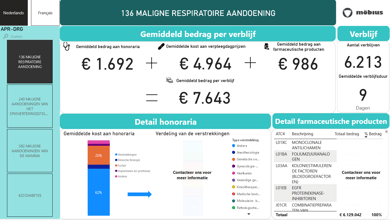

Interactive dashboard handling real-world data in HTA

Uncover the power of data analytics in healthcare! Learn how Möbius' interactive dashboard handles real-world data in health technology assessments (HTA) t…

Article

The Net Promoter Score (NPS) vs Customer Effort Score (CES)

Discover the differences between the Net Promoter Score (NPS) and Customer Effort Score (CES) in measuring customer satisfaction and loyalty.

No results found.

Searching ...

1

2

3